COMPETITIVE ENVIRONMENT

Exploration and Production

In 2019, domestic production of natural gas in Poland was approximately 42.5 TWh, of which 0.7 TWh was produced by PGNiG’s competitors (mainly FX Energy Poland Sp. z o.o. and the ORLEN Group). The share of the competitors in domestic production remained at 1.5% compared with 2018. The production volume of high-methane grid gas was close to 24.6 TWh.

Trade and Storage

PST’s main competitors are commodity trading companies (Vitol, Trafigura, Trailstone and others), which generally apply an opportunistic approach to entering the energy trading market. Their presence is seen in particular on the LNG market, where oversupply is expected in the coming years (2020–2022) because of new liquefaction capacities in the US.

On the Polish natural gas retail market, the company competes with the largest electricity suppliers that expand their operations to include sale of natural gas. Major competitors on the gas market in 2019, and the most active ones, were: SIME Polska Sp. z o.o., Fortum Marketing and Sales Polska S.A., TAURON Polska Energia S.A., Enea S.A., Axpo Polska Sp. z o.o. and Hermes Energy Group S.A. (declared bankrupt as at 01.12.2019).

In the LNG retail market, the main competitors are: DUON Dystrybucja Sp. z o.o.; NOVATEK Polska Sp. z o.o.; CRYOGAS M&T POLAND S.A., BARTER Sp. z o.o., Shell Polska Sp. z o.o. and Gaspol S.A.

PST ES’s main competitors on the retail market are large companies (E.ON, RWE, EnBW, Vattenfall) and municipal utilities owned by local authorities – all fighting to maintain or increase their market share in the end customer sector.

Distribution

There are 52 competing DSOs (Distribution System Operators) on the Polish gas distribution market, including:

- 19 entities for whom DSO activities are their core business, including 4 entities operating in closed distribution zones,

- 33 entities engaging in DSO activities outside their core business, including 29 entities operating in closed distribution zones.

In total, competing DSOs and entities engaged in LNG regasification (without a gas distribution licence) operate in 278 municipalities; competing DSOs and PSG operate in 133 municipalities.

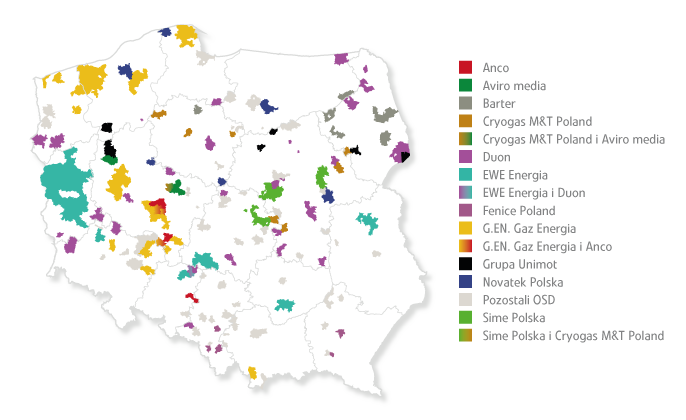

Operating areas of competitors in Poland

Source: In-house analysis based on PSG data.

Number of municipalities where competitors operate

* UNIMOT System Sp. z o.o. and Blue LNG Sp. z o.o.

** Other DSOs operating in two or fewer municipalities.

Among companies that have the largest influence on the Polish distribution market are entities with the majority of entry points into their distribution systems, including LNG regasification stations, being independent from PSG, which operate in approximately 40% of the municipalities where PSG’s has direct competitors. These include: DUON Dystrybucja Sp. z o.o.; GAZ ENERGIA Sp. z o.o., Novatek Polska. Other competitors are active on local markets or expand at smaller rates.

Generation

Heat

In the area of heat generation, PGNiG TERMIKA operates on markets limited by the boundaries of two separate municipal heating networks: in the capital city of Warsaw and in Pruszków, Piastów and Michałowice. A share in the heat production in Warsaw and a share in Pruszków makes PGNiG TERMIKA a natural monopolist in these areas. With respect to heat generation, its only true competitor is Zakład Utylizacji Stałych Odpadów Komunalnych of Warsaw (ZUSOK). A significant area of competition is sales of heat to end users, where the company operates under the TPA (third-party access) rules.

Electricity

PGNiG TERMIKA sells electricity almost exclusively on the wholesale market (with an only marginal share of sales to end customers). In 2019, as in previous years, the main players on the wholesale market were three groups of companies: PGE, TAURON, and ENEA, which account for some 67% of total installed capacity and whose electricity outputs represent approximately 70% of the total domestic production (the percentage figures are given for 2018 because the annual report on the operation of the Polish National Power System is not available). The PGE Group holds the largest share in electricity generation (2018: 42.9%). Given their shares in the wholesale market, the above entities certainly have a major impact on the development of energy prices in futures contracts.